Africa’s micro-retail sector is undergoing a digital transformation, reshaping how small, informal shops operate. With over 90% of the continent’s $1.4 trillion retail economy running through these small, family-run stores, digitization is unlocking new opportunities for growth. Here’s what’s driving this shift and how platforms like Chari are leading the charge:

- Mobile Connectivity Boom: Smartphone adoption is set to reach 88% by 2030, with over 527 million Africans already connected to mobile internet.

- Digitization of Small Shops: 93% of small businesses in Sub-Saharan Africa have digitized at least one part of their operations, enabling faster, more efficient processes.

- Chari’s Role: Chari has digitized over 20,000 shops in Morocco, offering tools like a B2B e-commerce app for inventory, digital payment solutions, and bookkeeping tools.

- Financial Inclusion: By integrating services like microloans, mobile wallets, and Visa cards, Chari helps unbanked shopkeepers access credit and manage finances digitally.

- Economic Impact: Shops using digital tools report a 50% increase in trading volume and frequency, driving growth in local economies.

This shift is not just about technology; it’s about equipping small retailers with tools to thrive in a changing market. Platforms like Chari are blending digital tools with local practices, transforming these shops into hubs for financial services and community growth.

Transforming the Informal Retail Market in Africa with Boost

sbb-itb-dd089af

How Chari Is Changing Micro-Retail

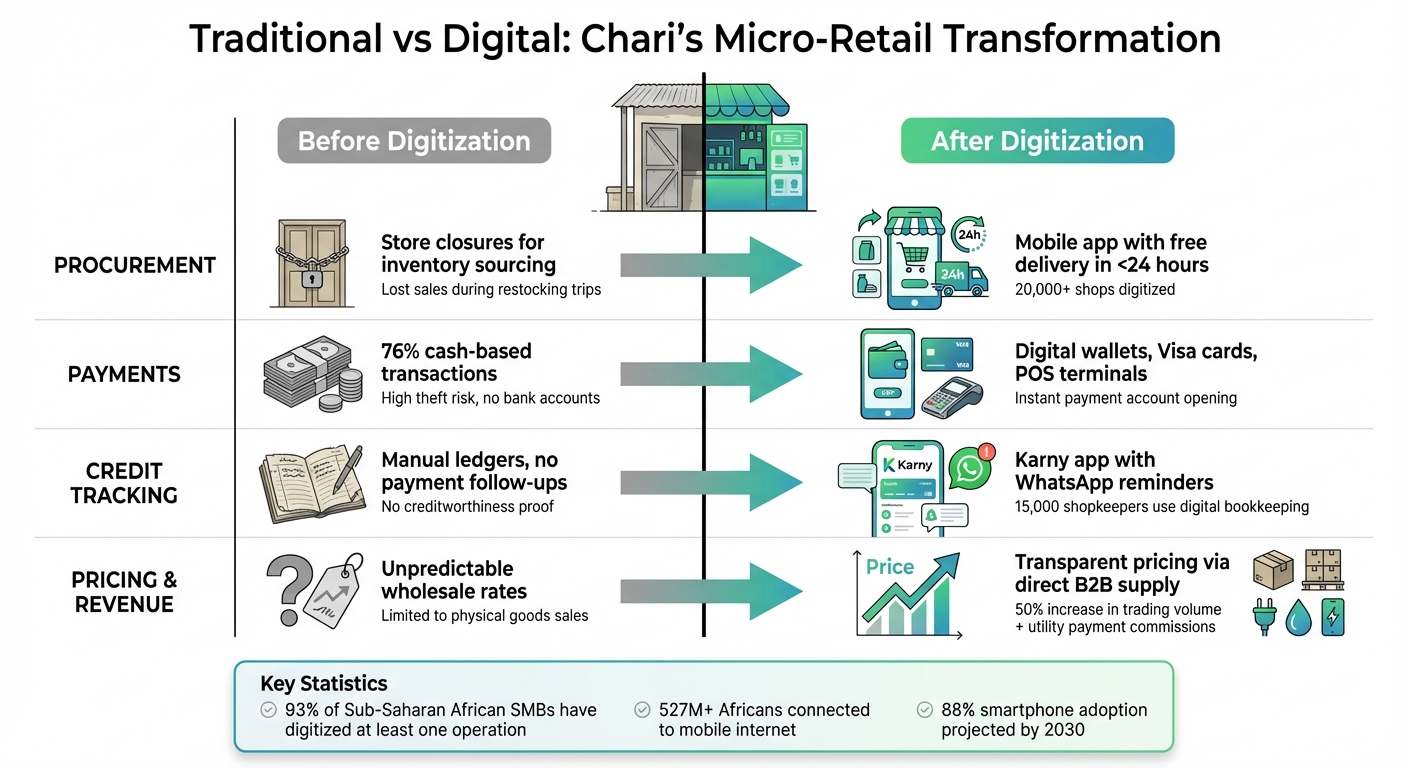

How Chari Digitizes African Micro-Retail: Before vs After Transformation

Chari, founded by CEO Ismael Belkhayat and co-founder Sophia Alj, is revolutionizing Morocco’s neighborhood shops by bringing them into the digital age. The platform has already digitized over 20,000 local shops, focusing on Morocco’s informal retail sector, which handles 80% to 85% of the country’s consumer goods distribution. Traditionally, shopkeepers had to close their stores and travel to wholesalers for restocking. Chari flips this outdated system by delivering the supply chain directly through a mobile app, reflecting a broader shift in Africa’s retail landscape.

Chari operates on a straightforward buy-and-sell model, purchasing goods from suppliers and reselling them with transparency. This system allows the company to maintain control over inventory quality and delivery while earning a 10% margin on transactions. By early 2026, Chari had raised $12 million in Series A funding – the largest funding round of its kind in Morocco at the time.

Chari’s Main Features for Retailers

Chari addresses critical pain points for micro-retailers with three key services.

- B2B e-commerce app: Shop owners can order fast-moving consumer goods with free delivery in under 24 hours. This eliminates the need for store closures during business hours to restock inventory.

- Embedded financial services: Retailers can open digital payment accounts in seconds, access Visa cards for business needs, and apply for microloans based on their transaction history. A partnership with Visa in April 2025 expanded Chari’s reach, helping digitize thousands of informal merchants across North Africa.

- Digital bookkeeping tools: Through its acquisition of the Karny app, Chari replaces traditional paper ledgers with a digital solution. Around 15,000 shopkeepers now use these tools at least twice a month to manage customer credit and receive automated payment reminders via WhatsApp.

| Feature | Traditional Challenge | Chari’s Solution |

|---|---|---|

| Procurement | Store closures for inventory sourcing | Mobile app with free delivery in <24 hours |

| Payments | Heavy reliance on cash; no bank accounts | Digital wallets, Visa cards, POS terminals |

| Credit Tracking | Manual ledgers; no payment follow-ups | Karny app with WhatsApp payment reminders |

| Pricing | Unpredictable wholesale rates | Transparent pricing via direct B2B supply |

By seamlessly integrating these services into daily operations, Chari makes it easier for shopkeepers to adopt modern tools without disrupting their workflows.

Connecting Informal Trade with Digital Tools

Chari taps into Africa’s growing mobile adoption to modernize micro-retail. In Morocco, where 76% of transactions are still cash-based and only 6% of adults use mobile wallets, forcing merchants to abandon familiar practices isn’t practical. Instead, Chari builds trust gradually.

"Once the independent retail shop owners use our service, they find out that we are a serious distributor that brings goods on time, at a good price with precise tracking… It is only when the shop owners trust us as a company, that they start using our financial services."

- Ismael Belkhayat, Founder and CEO, Chari

To address digital literacy challenges, Chari operates a 60-person call center to assist shopkeepers, including taking phone orders for those less comfortable with technology. One example is Ismail Berkouk, a 29-year-old unbanked shop owner in Casablanca. With help from Chari’s call center, he transitioned to using the app while continuing daily operations. He’s now exploring Chari’s upcoming mobile wallet.

Chari is evolving into a "merchant super app", where retailers can manage inventory, access working capital, process customer payments, and handle utility bills all in one place. By transforming local shops into hubs for financial services, Chari not only provides new revenue opportunities for merchants but also brings digital financial tools to unbanked communities.

"This is a unique opportunity to turn traditional grocery stores into local points of sale for financial services."

- Sophia Alj, Co-founder, Chari

How Chari Is Fixing SMB Payments

The Problem with Cash Dependency

In Morocco, cash dominates transactions, making up 76% of all exchanges. For micro-retailers, this reliance on cash brings a host of challenges. It exposes them to risks like theft, unauthorized use by employees, and the hassle of depositing funds. On top of that, keeping track of customer credit without proper records leaves these merchants unable to prove their creditworthiness. Traditional bank loans, often requiring substantial cash reserves or real estate as collateral, are out of reach for many.

This "cash trap" also forces shop owners to shut their doors just to visit wholesalers or endure long waits for distributor deliveries, leading to lost sales. The problem isn’t confined to Morocco – markets like Ghana see an even higher dependence on cash, with 99.9% of consumer goods payments still made this way.

Chari’s Payment Tools

Chari addresses these challenges head-on by integrating financial services into its B2B e-commerce platform. With a payment institution license from Morocco’s central bank, the platform enables merchants to open payment accounts instantly, cutting out tedious paperwork.

"We realized that access to products alone was not enough – these shop owners also needed financial solutions to keep their shelves stocked."

- Ismael Belkhayat, CEO and Co-Founder, Chari

Chari provides merchants with tools like Visa cards for business purchases, mobile wallets for digital payments, and POS terminals for in-store transactions. Its Karny bookkeeping app helps merchants digitize credit tracking for their customers, laying the foundation for credit scoring. This, in turn, allows them to access microloans without needing traditional collateral.

The platform doesn’t stop there. Merchants can also earn extra income by processing utility bill payments and mobile top-ups. Thanks to a partnership with Visa, Chari has extended its reach across North Africa, connecting thousands of informal merchants to global payment networks. These tools are reshaping how micro-retailers operate, offering solutions that were previously out of reach.

How This Improves Micro-Retail Operations

By tackling cash dependency and manual record-keeping, Chari empowers micro-retailers to modernize their operations. Take Ismail Berkouk in Casablanca, for example. Before March 2023, he managed his shop with nothing but paper ledgers. After adopting Chari’s platform, he began ordering inventory digitally, avoided closing his store for supply runs, and gained access to utility payment services – all while building a formal digital financial history.

| Feature | Before Digitization | After Digitization |

|---|---|---|

| Payment & Tracking | 76% cash-based; high theft risk; no formal records | Mobile wallets, Visa cards, and digital transaction tracking |

| Bookkeeping | Manual ledgers for customer credit | Digitized tracking via the Karny app |

| Credit Access | Requires high cash reserves or real estate guarantees | Credit scoring based on transaction history |

| Revenue Streams | Limited to physical goods sales | Expanded through utility bill payments and mobile top-ups |

Chari’s solutions are not just about convenience – they’re about giving micro-retailers the tools they need to thrive in an increasingly digital economy. By simplifying payments and introducing financial services, Chari is transforming the day-to-day operations of small businesses.

What African Startups Can Learn from Chari

Using AI to Optimize Operations

Chari’s success shows how startups can use AI to streamline operations effectively. For example, integrating conversational interfaces in local languages like Hausa, Swahili, or Arabic can make tools more accessible. Imagine a merchant asking, "Should I restock this?" and receiving tailored advice based on sales trends.

AI also plays a big role in predictive inventory management. By analyzing sales data, it can recommend when and how much to reorder, helping merchants avoid stockouts without needing to dive into complex analytics. Another practical feature? Allowing merchants to simply snap a photo of an item to find it, eliminating the hassle of text-based searches.

"The AI doesn’t just report; it advises. Effectively, they get an educated personal assistant who helps them participate in a more functionally optimal market without needing to learn anything new." – Samson Odo, Paylo

Beyond inventory, AI supports alternative credit scoring for Buy Now, Pay Later (BNPL) financing. Chari’s acquisition of the Moroccan bookkeeping app Karny in 2021–2022 was a game-changer, enabling the collection of transaction data to build these credit scores. Startups can take a page from Chari by focusing on tools that cater to low literacy levels, such as voice and visual interfaces. And because connectivity isn’t always reliable, ensuring offline functionality is crucial.

Building Last-Mile Logistics Partnerships

Chari’s logistics approach underscores the value of asset-light models in African markets. Instead of investing heavily in fleets and warehouses, startups can collaborate with third-party logistics (3PL) providers. These partnerships reduce costs while tapping into local expertise for the final delivery mile.

Chari makes ordering easy for shopkeepers by offering digital and phone channels, which even work on older devices. Early on, the company bought goods from cash-and-carry outlets at no profit, simply to gather data on buying patterns. This data later helped Chari prove its market presence to big manufacturers like P&G and L’Oréal, securing direct supply deals and improving profit margins.

"What they [shopkeepers] wanted was a simple app with big buttons." – Ismael Belkhayat, Co-founder and CEO, Chari

Expanding into West Africa in 2022, Chari acquired Diago, an Ivorian startup, to gain immediate access to Côte d’Ivoire’s market. This move bypassed the need to build logistics networks from scratch. For startups, the lesson is clear: rely on local couriers who know the terrain, group orders by location to save on fuel, and set clear agreements with logistics partners to maintain service quality. These logistics strategies, combined with financial innovations, create a well-rounded ecosystem for micro-retailers.

Community-Based Lending Models

Traditional banks often require high collateral, leaving micro-retailers without access to credit. Chari tackled this by digitizing informal credit records through its acquisition of Karny, building alternative credit scores from community-level data.

Trust is a cornerstone of Chari’s approach. The company focuses on earning credibility before introducing financial services.

"It is only when the shop owners trust us as a company, that they start using our financial services. Indeed, in some countries, many of these shops don’t pay taxes and are afraid to record any kind of online transactions." – Ismael Belkhayat, Founder, Chari

Chari also empowers local shops by turning them into financial hubs, enabling services like bill payments and mobile top-ups, which provide extra income streams. In April 2025, Chari partnered with Visa to bring secure electronic payment options to thousands of informal retailers in North Africa. The takeaway for startups? Focus on digitizing existing behaviors instead of trying to introduce entirely new ones. Support merchants with low digital skills through hands-on onboarding, such as call centers, and tailor solutions to local needs. Building trust through these steps ensures long-term success.

Case Studies: Chari in Action

Efficiency Gains for SMBs

Take Ismail Berkouk, for example – a snack shop owner in Casablanca. Before Chari, running his store meant closing up shop just to restock supplies from wholesalers. Now, he orders everything online and gets it delivered within 24 hours. No more lost sales or downtime. Plus, as an unbanked merchant, Berkouk is looking forward to using Chari’s mobile wallet to handle utility bill payments seamlessly.

Chari’s reach is impressive: the platform has digitized operations for over 20,000 small shops across Morocco. Out of these, 15,000 shopkeepers actively use the app at least twice a month to restock inventory. With free 24-hour delivery guaranteed, Chari has become a game-changer for these businesses. But it doesn’t stop at inventory. Chari’s financial tools turn shopkeepers into local financial hubs, enabling them to earn commissions on mobile top-ups, utility payments, and money transfers. And since acquiring Karny, a bookkeeping app, in August 2021, Chari now has access to transaction data from over 50,000 merchants. This move opens doors to credit scoring and Buy Now, Pay Later options tailored for retailers.

These operational improvements are the backbone of Chari’s plans to expand into new territories.

Expanding Across Multiple Markets

Chari’s success in streamlining operations has paved the way for regional growth. In June 2022, the company acquired Diago, a B2B e-commerce app in Côte d’Ivoire, gaining direct access to local entrepreneurs with deep market insights. Additionally, Chari has expanded into Tunisia, aiming to strengthen its presence across Francophone Africa.

What’s Next for African Micro-Retail

AfCFTA and Cross-Border Trade

The African Continental Free Trade Area (AfCFTA) is a game-changer. Covering 55 countries and over 1.3 billion people, it has the potential to create the world’s largest single market. But it’s not just about cutting tariffs – it’s about unifying digital payment systems, streamlining customs procedures, and improving data governance across borders.

Right now, fragmented regulations make expansion costly and complicated. AfCFTA’s digital trade protocol aims to fix this by standardizing payment systems and compliance rules. For companies like Chari, this could be huge. It means they could roll out data-driven financial services, like embedded credit, across multiple countries without having to build separate frameworks for each one.

The potential is massive. Mobile payment revenue in Africa is projected to hit $14 billion to $20 billion by 2025, with up to 850 million users generating $2.5 trillion to $3 trillion in transaction volume. However, there’s still work to do. Mobile money networks and banks often don’t “talk” to each other, making it hard for a shopkeeper in one city to accept payments from a customer using a different mobile wallet.

"Digital interoperability creates a remote settlement and clearing hub between the mobile wallets of mobile money subscribers and banks that strike a balance to meet instant demand and supply of money for trade."

- George Okello Candiya Bongomin, AIB Insights

As regulatory frameworks align, technology will play an even bigger role in fine-tuning how micro-retailers operate.

AI and Personalization at Scale

AI is changing the game for micro-retailers, making once-complex business decisions much simpler. It turns mountains of data into clear, actionable insights. For example, if a retailer searches for a supplier in their native language, AI can instantly match them with a nearby wholesaler offering the best price and fastest delivery. This gives small businesses a leg up, prioritizing quality and proximity instead of relying on flashy advertising.

Platforms are now embedding AI directly into their systems. For Chari, this means using transaction data to predict demand, fine-tune restocking schedules, and identify merchants who could benefit from services like Buy Now, Pay Later. But there’s a catch – AI is only as good as the data it’s fed. Clean, well-organized inventory and transaction records are critical to making these recommendations reliable.

"Language is no longer a barrier to accessing world-class business intelligence."

- Samson Odo, Founder, Paylo

These advancements are paving the way for faster e-commerce adoption across the continent.

E-Commerce Growth Projections

Africa’s e-commerce market is on the rise, expected to grow to $56.03 billion by 2029, with an annual growth rate of 8.46% between 2025 and 2029. Some forecasts even see it surpassing $1 trillion by 2033. Mobile transactions will be a driving force, projected to make up over 60% of e-commerce sales by 2025.

Smartphones are at the heart of this growth. By 2030, smartphone penetration is expected to jump from 50% in 2024 to over 80%. As Abdesslam Benzitouni, VP of Global Public Affairs at Jumia, puts it:

"Affordable smartphones and expanding internet access are bringing millions of Africans online, significantly boosting digital services and e-commerce."

For platforms like Chari, this growth isn’t just about selling products. It’s about offering a full suite of tools – bookkeeping, inventory management, and credit services. Take Kippa, for example. This Nigerian startup launched in 2021 and already serves over 500,000 merchants, facilitating more than $3 billion in annual transactions through its tools.

But challenges remain. Instant payment volumes reached over 64 billion transactions by 2024, with values nearing $2 trillion. To keep up, platforms must tackle fragmented payment systems and push for seamless interoperability between mobile money providers and banks. The ultimate goal? Making cross-border payments as easy as sending a text. These trends highlight the exciting trajectory of micro-retail, with companies like Chari leading the way toward a more connected and efficient future.

Conclusion: The Future of Micro-Retail with Chari

Chari has taken significant strides in reshaping Africa’s micro-retail landscape, digitizing over 20,000 small shops and creating a unified ecosystem that combines digital payments, logistics, and Banking-as-a-Service (BaaS). What began as a B2B e-commerce platform has evolved into a merchant super app, empowering traditional "mom-and-pop" stores to serve as neighborhood financial hubs. These shops now offer services like bill payments, fund transfers, and access to banking features that were once exclusive to formal financial institutions.

The impact of this transformation is already visible. Traditional retail contributes more than 70% of food, beverage, and personal care sales in Africa – a massive $600 billion informal market that Chari is helping to formalize. In April 2023, Chari became the first venture-backed startup in Morocco to secure a payment institution license from the central bank. This milestone allowed the company to build its own core banking system and offer a BaaS platform, enabling other businesses to integrate financial services using Chari’s infrastructure.

"Now that our rails are fully operational and supporting Chari’s needs, we are opening them to third parties. This marks the beginning of Chari’s Banking-as-a-Service (BaaS) offering."

- Ismael Belkhayat, CEO, Chari

Strategic collaborations are playing a key role in this journey. For example, in April 2025, Visa partnered with Chari to digitize thousands of informal merchants across North Africa. This partnership introduced global payment infrastructure into local corner shops, helping merchants transition from cash-heavy operations to secure electronic payments. By addressing liquidity and trust challenges, these efforts are modernizing micro-retail while preparing the ground for broader financial integration.

Chari’s ambitions extend far beyond individual shops. The company aims to support regional economic integration through initiatives like the African Continental Free Trade Area (AfCFTA). By standardizing B2B e-commerce and fintech services across borders, Chari is setting the stage for scalable cross-border remittances and domestic transfers. With operations in Morocco, Tunisia, and Côte d’Ivoire – and plans to expand further into West Africa – the company is building a financial infrastructure that connects fragmented markets. In regions like Kenya, where 97% of small retailers already use mobile money, Chari’s model could provide the missing framework to unify and scale these digital efforts.

FAQs

How does digitization help a small shop grow profits?

Digitization helps small shops increase profits by simplifying operations and reaching more customers. With digital tools, inventory management becomes more efficient, often allowing for quicker deliveries and fewer stockouts, which minimizes downtime. These tools also enhance cash flow, cut transaction costs, and even open up access to credit, which can fuel growth.

On top of that, digital payment options bring in more customers who prefer cashless transactions. Plus, the data collected from these transactions can be used to fine-tune pricing and inventory strategies, helping shops stay competitive and boost profitability.

What does a merchant need to start using Chari?

To get started with Chari, merchants need a digital device, such as a smartphone or tablet, and must complete the registration process on the platform. After signing up, they can place orders for FMCG products, process digital payments, and make use of financial services. This setup simplifies their workflow and helps make daily operations smoother.

How can transaction data unlock microloans for unbanked retailers?

Transaction data plays a key role in helping unbanked retailers gain access to microloans. By analyzing their transactional records, credit scoring models can assess their ability to repay loans, even if they don’t have a traditional credit history. This method opens the door to formal credit for retailers who might otherwise be excluded due to a lack of standard financial documentation.

Related Blog Posts

- 8 Solutions to Common African E-commerce Challenges

- Top 7 Mobile-First E-Commerce Startups in Africa

- Future of Mobile Money in African Marketplaces

- How to Build a Scalable Tech Product with a Small Team in Africa