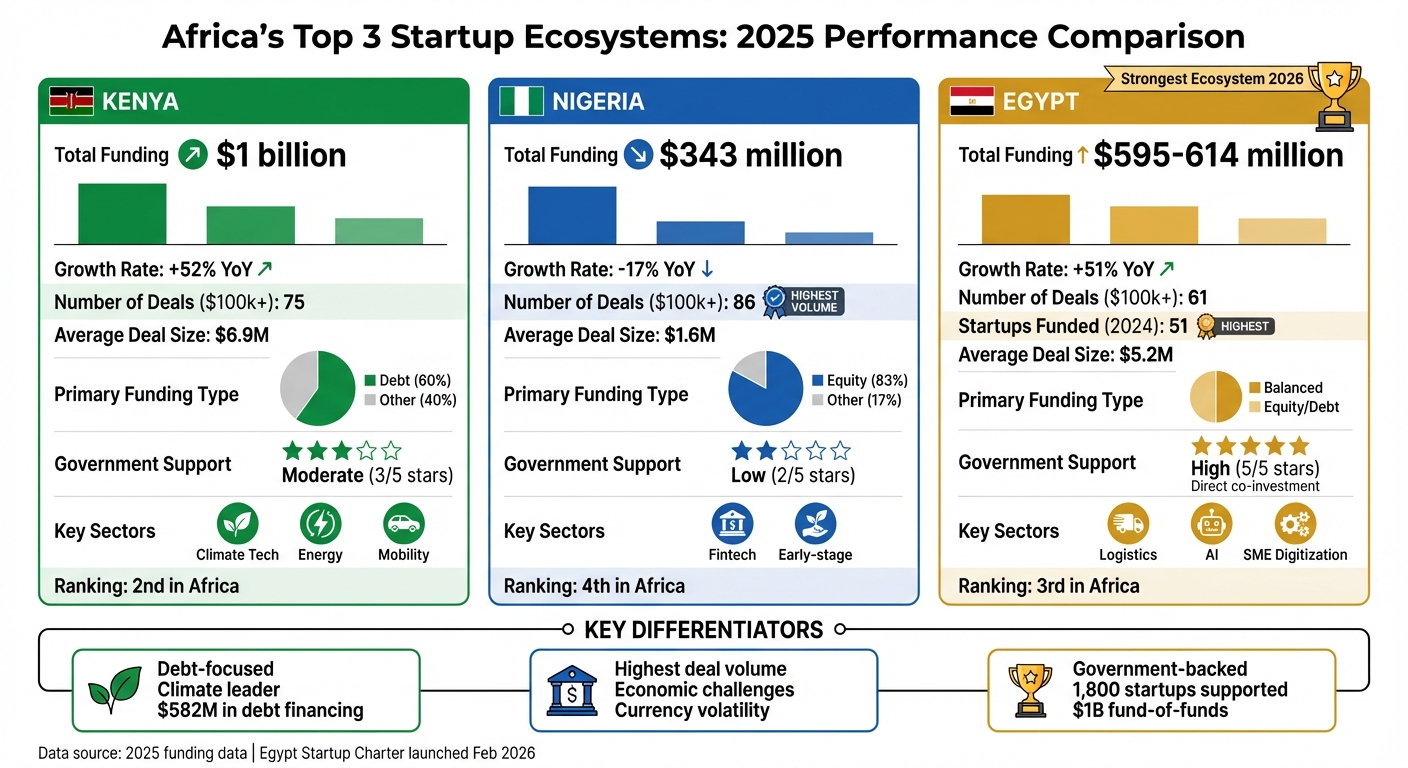

Egypt leads Africa’s startup ecosystems in 2026. With a mix of government-backed funding, streamlined policies, and a growing tech sector, Egypt outpaces Kenya and Nigeria in creating a balanced environment for startups. Kenya excels in climate-focused ventures and large-scale funding, while Nigeria boasts the highest deal volume but struggles with economic instability.

Key Highlights:

- Egypt: $595M raised in 2025 (+51% growth). Strong government support with direct co-investment, tax benefits, and tech parks.

- Kenya: $1B raised in 2025 (+52% growth). Focus on climate tech, but funding is concentrated in fewer startups.

- Nigeria: $343M raised in 2025 (-17% decline). High deal volume but economic challenges hinder growth.

Quick Comparison:

| Metric (2025) | Egypt | Kenya | Nigeria |

|---|---|---|---|

| Total Funding | $595M | $1B | $343M |

| Growth Rate | +51% | +52% | -17% |

| Avg. Deal Size | $5.2M | $6.9M | $1.6M |

| Government Support | High | Moderate | Low |

| Focus Areas | Logistics, AI | Climate Tech | Fintech |

Egypt’s balanced approach, combining public and private investment, positions it as the most resilient ecosystem for startups in 2026.

Kenya vs Nigeria vs Egypt Startup Ecosystem Comparison 2025-2026

The Future of the African Startup Ecosystem | Investment & Growth Trends | Afribond

sbb-itb-dd089af

Kenya’s Startup Ecosystem in 2026

Kenya emerged as Africa’s leader in startup funding in 2025, raising an impressive $984 million – a 52% jump from the previous year – claiming about one-third of all startup investments across the continent. However, this growth wasn’t evenly distributed. Debt financing took the lead, accounting for $582 million (60% of the total), while equity funding nearly doubled to $383 million. This trend highlights a shift among mature startups toward loans to retain ownership. These funding patterns reflect Kenya’s growing strength in tech and innovation.

A significant portion of this funding came from a handful of energy and climate-focused companies. Five key players – d.light, Sun King, M-Kopa, Burn, and PowerGen – secured 82% of the total funding. Beyond raising capital, these companies are also investing in local manufacturing. For instance, M-KOPA operates one of Africa’s largest smartphone assembly plants in Nairobi, producing over 2 million devices and transforming a $20 million loss into a $9.2 million profit in 2025. Similarly, Sun King’s facility, capable of assembling over 700,000 solar-powered units annually, now serves one in five Kenyan households.

Key Strengths

Kenya’s financial successes are underpinned by several strategic advantages. M-Pesa plays a pivotal role in the country’s digital economy, with over 83% of adults accessing formal financial services via mobile money platforms. This robust digital infrastructure has made Kenya a magnet for global tech giants like Microsoft, Google, and Visa, all of which have established regional R&D hubs in Nairobi. On top of this, companies like BasiGo are advancing Kenya’s electric vehicle industry. By late 2025, BasiGo had expanded its electric bus assembly line in Thika, deploying over 70 buses and securing $60 million in funding to meet its goal of 1,000 buses by 2027.

Other factors boosting investor confidence include widespread smartphone adoption, regulatory sandbox frameworks, and a focus on sustainable unit economics over unchecked growth. In 2025, Eastern Africa – led by Kenya – secured 34% of all funding across the continent. Globally, Kenya’s startup ecosystem ranks 58th and has grown by 33.5% over the past year.

Challenges

Despite these achievements, systemic challenges persist. The number of startups securing significant funding has dropped. In 2025, only 75 Kenyan ventures raised $100,000 or more – a 23% decline – while Nigeria outpaced Kenya with 86 deals in the same period. This indicates a growing concentration of capital among fewer players.

Government support, while present, remains disorganized. Unlike Egypt’s centralized ITIDA model, which supports 1,800 startups, Kenya’s programs lack coordination. Founders often face excessive bureaucracy and paperwork when seeking government funding. The proposed Startup Act, which could streamline these processes, is still under debate. Meanwhile, existing programs like the Youth Enterprise Development Fund operate more like traditional loan schemes than modern startup accelerators.

Infrastructure issues also pose challenges. Frequent power outages can increase operating costs for small businesses by up to 25%, forcing startups to invest in expensive backup systems. Additionally, Kenya is grappling with a brain drain, as skilled tech talent often migrates to Europe or North America for better opportunities. A $330 billion credit gap for MSMEs further limits access to essential working capital. These obstacles threaten to erode Kenya’s competitive position in Africa’s startup landscape.

"Kenya’s government support is fragmented, inconsistent, and often trapped in bureaucracy." – Bolu Babalola, Techmoonshot

Nigeria’s Startup Ecosystem in 2026

Once a leader in startup funding, Nigeria now ranks fourth among Africa’s Big Four, falling behind Kenya, South Africa, and Egypt. In 2025, Nigerian startups raised $572 million, marking a 3% drop that reduced its share of total African funding to 11%.

The numbers paint a challenging picture. Nigeria led the continent in deal volume with 205 transactions in 2025. However, the average deal size was just $1.6 million – significantly lower than Kenya’s $6.9 million and South Africa’s $9.2 million. Adding to this, Nigeria had no megadeals in 2025, while Kenya closed four major rounds in energy and climate tech.

Economic instability has also taken its toll. By early 2026, the naira had devalued to approximately ₦1,420 per $1, with inflation soaring to 25–30%. This has eroded consumer purchasing power and made the environment less appealing to investors.

"Africa’s tech capital has moved. And Nigeria let it happen." – Betty Wangari, Techmoonshot

Despite these hurdles, Nigeria remains a leader in deal volume and continues to boast a strong fintech sector. With a population of over 200 million, the market potential is enormous. Yet, the ecosystem’s heavy reliance on equity funding – accounting for 83% of total funding – makes it more susceptible to global funding slowdowns compared to markets leveraging venture debt. Even so, fintech remains a driving force for innovation in the country.

Key Strengths

Nigeria’s fintech sector is a standout, leading advancements in payments, lending, and neobanking. In 2025, Moniepoint secured a $90 million Series C extension. The sector’s scale is evident, with electronic payments reaching ₦1.07 quadrillion (around $753 billion) in 2024.

The Nigerian Startup Act is another bright spot, offering tax incentives, regulatory clarity, and support mechanisms aimed at fostering entrepreneurship. Lagos, the country’s tech hub, hosts over 120 active AI startups, showcasing a pool of technical talent and entrepreneurial drive. Additionally, Nigeria’s large market size and widespread mobile penetration create fertile ground for scaling businesses. Early-stage startups like Washr, which connects users to vetted service providers, highlight the ecosystem’s ongoing innovation.

Challenges

One major issue is funding concentration. In 2024, over half of Nigeria’s total funding came from just two deals – Moove and Moniepoint. Infrastructure remains a persistent problem, with more than 60% of the population lacking reliable electricity. Startups are often forced to invest in expensive backup power solutions. Poor internet connectivity and outdated equipment in grassroots tech hubs further hinder operations.

Regulatory uncertainty adds to the difficulties. For example, the Securities and Exchange Commission increased capital requirements by 3,900% in some categories, creating significant barriers for startups. While the Nigerian Startup Act offers a framework for growth, founders have reported challenges in its implementation, such as complex "Startup Label" requirements and limited fund deployment.

Another concern is the ecosystem’s heavy focus on fintech. As global investors shift their attention to sectors like climate tech and AI, Nigeria has struggled to adapt. Fintech’s share of African equity funding dropped from 60% in 2022 to 25% in 2025, and the country has yet to secure major deals in energy, despite widespread electricity shortages.

Lastly, brain drain is taking its toll. Many talented founders are incorporating offshore in places like Delaware or Mauritius or relocating entirely to escape naira volatility and regulatory challenges.

Egypt’s Startup Ecosystem in 2026

Egypt is taking a unique approach to building its startup ecosystem, with the government playing a central role as both a co-investor and an infrastructure provider. In February 2026, the country introduced the Egypt Startup Charter – a roadmap involving 15 national entities aimed at reducing bureaucratic hurdles and attracting $5 billion in venture capital by 2031. This initiative marks a pivotal moment for the country’s startup landscape.

In 2025, Egyptian startups raised $595 million, reflecting a 51% year-over-year increase and placing Egypt third in Africa for funding. The country also led the continent in 2024 with 51 VC-funded startups, surpassing Kenya’s 28 and Nigeria’s 39. The ICT sector, which contributes 5.8% to Egypt’s GDP, continues to be the fastest-growing segment.

A standout feature of Egypt’s strategy is its "government-as-platform" model, which actively supports startups through programs like the "Start IT" incubator. This initiative, now in its 47th round, has helped launch 1,800 startups and created 31,000 jobs. In January 2026, fintech startup Flend secured seed funding with direct equity participation from MSMEDA (the state enterprise agency) and Banque Misr, alongside private investors. This highlights how the government is bridging funding gaps for early-stage ventures.

"Egypt is playing a different game. They’re not optimizing for unicorns; they’re optimizing for employment, tax revenue, and sustainable economic growth." – Bolu Babalola, Tech Analyst, Techmoonshot

A Broadening Focus

While fintech remains a dominant sector, led by unicorn MNT-Halan, Egypt is expanding into areas like e-commerce, healthtech, and AI. Cairo is home to roughly 510 startups, accounting for 90% of the national total. The MaxAB and Wasoko merger, which created a retail network serving 450,000 merchants regionally, underscores Egypt’s emerging role as a hub for scaling businesses.

Key Strengths

Egypt’s startup ecosystem benefits from a range of government-led initiatives that set it apart from competitors like Kenya and Nigeria. These include:

- Funding Security: The Unified Financing Initiative established a $1 billion fund-of-funds managed by MSMEDA. This fund supports venture debt and provides matching funds for angel and corporate investors, reducing risks for private participants.

- Infrastructure: The country operates six Technology Innovation Parks, with four already functional, offering subsidized facilities and access to skilled talent.

- Procurement Opportunities: Startups and SMEs are guaranteed 40% of government procurement contracts, with a 15% price preference for local firms.

- Regulatory Reforms: The 2026 Startup Charter introduced a digitalized one-day incorporation process and a 90-day liquidation mechanism, streamlining operations for businesses. Startups earning up to EGP 20 million (around $400,000) annually enjoy fixed income tax rates of 0.4–1.5% and exemptions from capital gains and stamp duties.

"The charter’s enforcement would mean the end of regulatory ambiguity. By formally recognizing startups as a distinct category, the government eliminates major friction around registration, taxation, and compliance." – Mazen Nadim, Managing Partner, Foundation Ventures

Egypt also stands out for its diverse funding options. Unlike Kenya and Nigeria, where equity funding dominates, Egyptian startups are increasingly leveraging venture debt and securitized bonds. In 2025, bonds and institutional debt made up nearly 30% of total funding. The country also led Africa in strategic exits, accounting for almost one-third of all acquisitions on the continent that year.

Challenges

Despite its progress, Egypt’s ecosystem faces some hurdles:

- Heavy Reliance on Government: While state involvement ensures stability, it also raises concerns about cronyism and political interference. Scaling government programs to support thousands of ventures without compromising quality is a challenge.

- Economic Instability: The Egyptian pound lost over 50% of its value between 2022 and 2026, creating financial uncertainty for startups. This currency volatility weakens consumer purchasing power and complicates long-term planning.

- Limited Private Sector Role: While Egypt has built a strong base of mid-sized tech companies, attracting more international private capital is crucial for scaling globally competitive ventures. The government’s goal of cultivating five unicorns by 2031 will require a more robust private VC ecosystem. Without this, Egyptian startups may struggle to compete with better-funded counterparts in sectors like climate tech and AI.

Egypt’s startup ecosystem is undoubtedly growing, but balancing state involvement with increased private sector participation will be key to sustaining this momentum.

Head-to-Head Comparison

Comparison Table

| Metric (2025 Data) | Kenya | Nigeria | Egypt |

|---|---|---|---|

| Total Funding | ~$1 billion | ~$343 million | ~$614 million |

| Year-on-Year Growth | +52% | -17% | +51% |

| Number of Deals ($100k+) | 75 | 86 | 61 |

| Average Deal Size | $6.9 million | $1.6 million | $5.2 million |

| Primary Funding Type | Debt (60%) | Equity (83%) | Equity/Debt Split |

| Startups Funded (2024) | 28 | 39 | 51 |

| Government Support Model | Policy/Incubation | Tax holidays + Seed Fund | Direct co-investment |

| Key Sector Focus | Climate/Energy/Mobility | Fintech/Early-stage | Logistics/SME Digitization |

Analysis

The comparison table highlights how Kenya, Nigeria, and Egypt have carved out distinct paths in their startup ecosystems. Each country’s strategy reflects its unique priorities and challenges.

Kenya’s approach leans heavily on debt financing, which makes up 60% of its funding. This strategy supports fewer but larger deals, with an average size of $6.9 million, particularly in asset-backed sectors like clean energy and mobility. This focus has helped Kenya attract about 33% of all funding across the continent in 2025, reinforcing its reputation as a stable destination for growth capital.

Nigeria, on the other hand, prioritizes volume. With 86 deals exceeding $100,000 in 2025, Nigeria leads in transaction count. However, its average deal size of $1.6 million is the smallest among the three, and total funding fell 17% year-over-year to $343 million. This suggests that while Nigeria’s ecosystem remains active, investor confidence may be waning, partly due to currency instability and perceived risks.

"Capital is more selective, risk appetite more measured, and growth expectations more realistic." – Dario Giuliani, Founder and Managing Director, Briter Intelligence

Egypt takes a balanced route, combining private capital with direct government involvement. The state co-invested in at least seven early-stage deals in 2025, while funding 51 startups in 2024 – the highest number in Africa. This hybrid model fosters a broad base of mid-sized companies, focusing on logistics and SME digitization rather than chasing high-risk, high-reward unicorns.

One of the biggest trends shaping these ecosystems is the pivot toward profitability. Debt financing surpassed $1 billion across Africa in 2025, as startups in sectors like energy and logistics turned to loans to avoid diluting equity. At the same time, mega-rounds exceeding $50 million accounted for less than 5% of deals but captured half of all disclosed funding. This concentration reflects a growing preference for backing established players over riskier ventures.

Geographically, investor sentiment is shifting. Kenya and Egypt are increasingly seen as safer bets for growth capital, while Nigeria’s high deal volume comes with heightened risks tied to economic volatility. These dynamics not only explain the funding disparities but also highlight the opportunities and challenges that will shape 2026’s investment landscape.

Which Country Has the Strongest Startup Ecosystem in 2026?

Egypt stands out as the leader in the startup ecosystem for 2026, thanks to its unique blend of state-backed infrastructure and private investment. Unlike Kenya’s focus on funding or Nigeria’s heavy transaction volumes, Egypt takes a more balanced approach by fostering a diverse range of mid-sized tech companies. This strategic emphasis positions Egypt as the most stable and forward-looking ecosystem heading into 2026.

Programs like ITIDA and TIEC have been instrumental in Egypt’s success, supporting 1,800 startups and creating 31,000 jobs. A notable milestone came in February 2026 when Flend became the first startup to earn Egypt’s National Startup Label. Flend also secured seed funding that combined government equity investments from MSMEDA and Banque Misr with private venture capital.

Egypt’s ecosystem offers clear advantages for both investors and entrepreneurs. For investors, the government’s co-investment approach reduces early-stage risks. On the other hand, Kenya remains a strong player in sectors like climate tech, which benefit from large-scale debt facilities. Entrepreneurs in Egypt can take advantage of initiatives like the "Start IT" incubation program, now in its 47th cycle. This program provides non-dilutive support, including $10,000 in AWS credits and free office space, making it a standout resource for startups.

Egypt’s integrated model – combining training, tech parks, and direct co-investment – serves as a blueprint for building resilient ecosystems. While Kenya excels in innovation readiness (ranked 68th globally and 2nd in Africa) and Nigeria boasts a massive market scale, Egypt’s well-rounded and comprehensive approach secures its place as the strongest startup ecosystem for 2026.

FAQs

What makes Egypt’s ecosystem more resilient than Kenya’s or Nigeria’s in 2026?

Egypt’s startup scene in 2026 is thriving, thanks to robust government backing and well-thought-out initiatives. A few standout elements include a $1 billion fund-of-funds, a "startup charter" aimed at energizing the tech industry, and Egypt’s top position in North Africa on the 2025 Global Startup Ecosystem Index. These measures have fostered an environment that supports growth and scalability. In contrast, markets like Kenya and Nigeria face challenges with funding and policies being heavily concentrated in limited sectors.

How do debt-heavy vs equity-heavy funding markets change startup risk and growth?

Debt-heavy funding can put startups under financial strain because of fixed repayment obligations, which might squeeze cash flow. However, it offers the advantage of enabling rapid growth without giving up ownership stakes. On the other hand, equity-heavy funding eases short-term financial pressure and supports steady, long-term development, though it comes at the cost of diluted ownership and meeting investor expectations for returns. In Africa, the growing use of both debt and equity funding showcases how each plays a unique role in fueling startup expansion and driving innovation.

Which country is best for my sector – climate tech, fintech, or AI?

The best country for your industry in 2026 will hinge on the strengths of its ecosystem. Egypt stands out in areas like climate tech and AI, thanks to robust government support and unprecedented funding levels. Kenya shines in fintech, boasting a well-established and vibrant ecosystem. Meanwhile, Nigeria presents enormous market potential and has introduced regulatory changes that favor sectors like AI and climate tech. Each of these nations brings distinct advantages, making the ideal choice heavily reliant on your specific industry focus.

Related Blog Posts

- African Tech Hub Comparison: Lagos vs Nairobi vs Cape Town

- Top 7 African Tech Hubs Building Communities

- Top 5 Startups to Watch in Kenya in 2025

- Kenya vs. Nigeria: Startup Funding Comparison