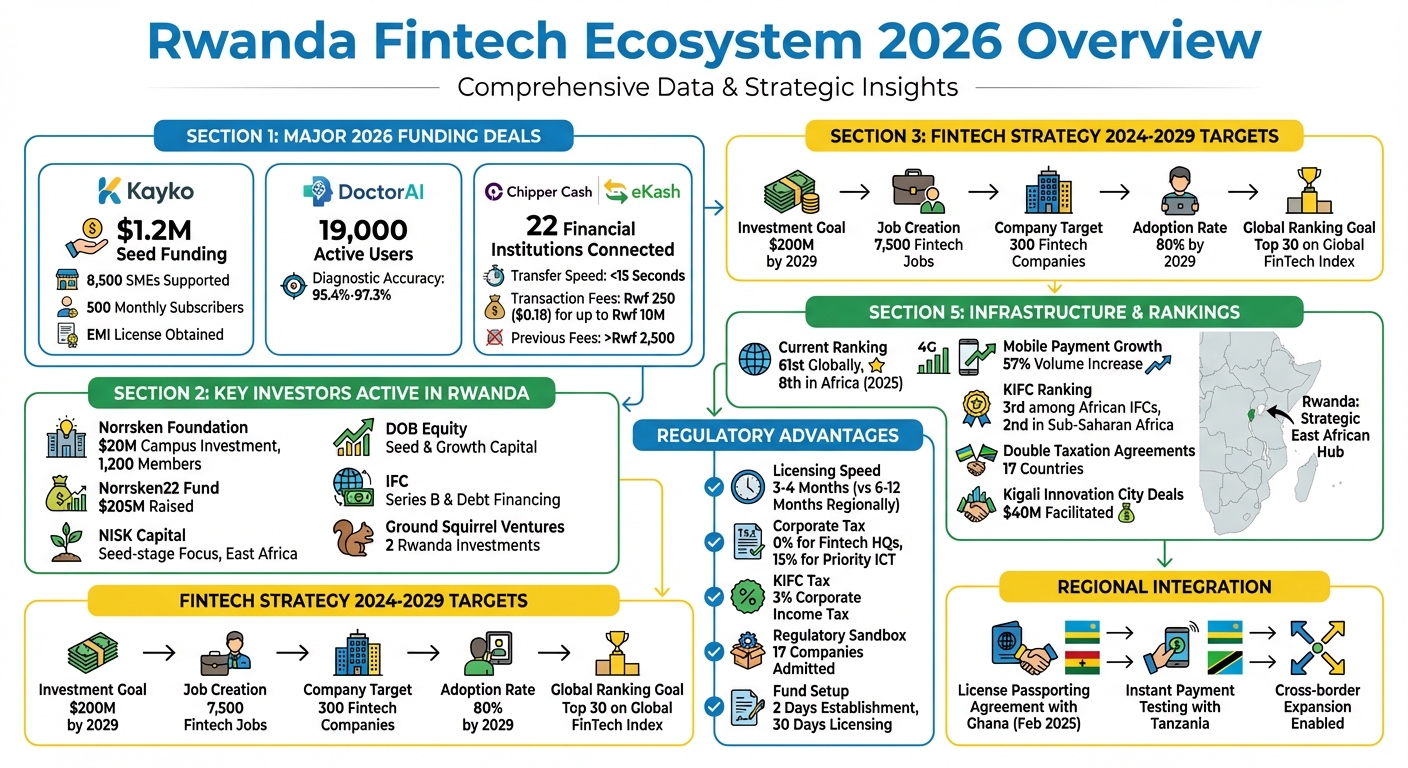

Rwanda is solidifying its position as one of Africa’s most dynamic fintech hubs. By leveraging forward-thinking policies, streamlined licensing, and digital infrastructure, Kigali has become a launchpad for startups targeting the African market. In 2026, major investments in fintech emphasized areas like SME digitization, healthcare payments, and cross-border financial services. Key highlights include:

- Kayko raised $1.2M to digitize SMEs and received an EMI license for regulated payments.

- DoctorAI integrated healthtech with fintech, serving 19,000 users with AI-driven diagnostics.

- Chipper Cash expanded with the launch of eKash, cutting transaction fees for instant payments.

Investors like Norrsken Foundation, NISK Capital, and DOB Equity are driving growth, while initiatives such as the Rwanda Digital Acceleration Program and Kigali International Financial Centre attract global attention. With a goal of $200M in fintech investments by 2029, Rwanda’s ecosystem is scaling rapidly, offering startups the tools to expand regionally.

Kigali’s success lies in its efficient regulatory framework, tax incentives, and infrastructure like nationwide 5G and digital ID systems, making it a standout destination for fintech innovation in Africa.

Rwanda Fintech Ecosystem 2026: Key Metrics, Investments, and Growth Targets

Fintech innovation boosts financial inclusion, Rwanda to host inclusive Fintech Forum 2026

sbb-itb-dd089af

Major Fintech Funding Deals in 2026

Rwanda’s fintech sector kicked off 2026 with an impressive start, as several key investments underscored the country’s ambition to become a regional financial powerhouse. These deals focused on areas like data-driven lending, SME digitization, and regulated payment systems, signaling Kigali’s growing reputation as a fintech hub.

Kayko Funding Round

In January 2026, Kayko, a Kigali-based fintech, secured $1.2 million in seed funding to digitize informal merchants and provide financial services to small and medium-sized enterprises (SMEs). Founded by brothers Crepin and Kevin Kayisire, Kayko now supports over 8,500 SMEs, with 500 of them subscribing monthly.

The funding round drew participation from Burrow Capital, the Luxembourg Development Agency (LuxDev), Hanga Ignite (by BRD), develoPPP Ventures, and a $500,000 investment from a South African angel investor. Kayko’s platform operates as a micro-ERP system, helping merchants transition from paper-based bookkeeping to digital records. This digital transformation enables banks to use transaction data for credit scoring, allowing SMEs to access loans without traditional collateral requirements.

Additionally, Kayko received an Electronic Money Issuer (EMI) license from the National Bank of Rwanda, allowing it to manage regulated payments and merchant wallets.

"With this license, we move from planning to execution. We can now operate regulated payments, merchant wallets, and data-driven financial services that improve access to financing for small businesses." – Crepin Kayisire, Co-founder, Kayko

Kayko’s early development was supported by the Rwanda Digital Acceleration Program (RDAP), a $200 million initiative backed by the World Bank and the Asian Infrastructure Investment Bank, which helped validate its business model.

DoctorAI Investment Details

DoctorAI, led by CEO and Co-founder Dr. Kevin Muragijimana, merges fintech and healthtech by integrating AI-driven diagnostic tools with financial services. The platform, which serves 19,000 active users, boasts diagnostic accuracy rates between 95.4% and 97.3%. While exact 2026 funding details remain undisclosed, the platform’s rapid growth has drawn significant investor interest.

DoctorAI combines medical insurance and financial services into a unified mobile app, creating a streamlined healthcare payments ecosystem that improves diagnostic accuracy and expands access to advanced medical resources.

"The DoctorAI Assistant integrates multiple specialized AI systems into a single, easy-to-use interface… reducing diagnostic errors and improving access to advanced medical knowledge." – Dr. Kevin Muragijimana, CEO and Co-founder, DoctorAI

MarketForce Series A Expansion

MarketForce, a company focused on retail digitization, has been expanding its operations in Rwanda as part of its East African growth strategy. The platform provides small retailers with tools for inventory financing, digital payments, and supply chain management.

Rwanda’s efficient licensing process, which now takes only 3–4 months compared to 6–12 months in other countries, has supported MarketForce’s entry and growth in the region.

Chipper Cash Growth Funding

Chipper Cash, a leading cross-border payment platform in Africa, continued its expansion in Rwanda in 2026. The company’s focus on remittances and peer-to-peer transfers has been bolstered by improved infrastructure, including the February 2026 launch of the eKash platform.

Operated by RSwitch, eKash connects 22 financial institutions – such as Bank of Kigali, Ecobank, MTN MoMo, and Airtel Money – enabling instant transfers of up to Rwf 10 million (roughly $7,300) in under 15 seconds. Transaction fees have dropped significantly, with transfers of up to Rwf 10 million costing as little as Rwf 250 (about $0.18), down from previous fees exceeding Rwf 2,500. Rwanda is also testing instant payment connections with Tanzania, setting the stage for regional interoperability.

These funding milestones highlight Kigali’s growing role as a launchpad for fintech innovation in East Africa. The ecosystem is maturing, with startups attracting a mix of development funding and commercial investment. In 2025, the Rwanda Development Bank (BRD) backed 22 companies and aimed to support 35 by year-end, reflecting increasing investor confidence.

"Strong performers in our portfolio proved us wrong – their user growth, revenue traction, and ability to attract follow-on investors showed there’s real room for commercial financing alongside catalytic support." – Magnifique Ishimwe, Rwanda Development Bank (BRD)

Together, these investments demonstrate how Kigali’s fintech startups are scaling rapidly, validating their business models, and expanding across East Africa.

Top Investors in Rwanda’s Fintech Sector

Rwanda’s fintech growth is backed by a mix of international development institutions, impact-driven foundations, and regional investment firms. Together, these players create a funding pipeline that supports startups from early validation through growth scaling. Let’s dive into the key investors shaping this space.

Ground Squirrel Ventures Portfolio

Ground Squirrel Ventures, based in Boston, zeroes in on frontier markets, particularly seed-stage opportunities in financial services and clean energy. They connect international capital with local startups in emerging economies. As of January 2026, the firm has made two investments in Rwanda. Their focus is on identifying businesses with potential for expansion across African markets.

Norrsken Foundation Investments

The Norrsken Foundation has become a cornerstone of Kigali’s fintech ecosystem. It invested $20 million into its 12,000-square-meter Kigali campus, which, by November 2023, housed around 1,200 members and hosted VC firms like Katapault and Angaza Capital. The foundation’s mission is to create “impact unicorns” – billion-dollar companies that deliver social and environmental benefits while remaining profitable.

Among its investments is Eden Care Medical, a Rwandan insurtech and the first local company to join YCombinator. Norrsken also organized Norrsken Africa Week in November 2023, drawing 1,500 entrepreneurs and investors. Additionally, Norrsken22, an associated fund, raised $205 million to support growth-stage tech firms across Africa.

"Rwanda is an excellent testbed and a proof-of-concept hub." – Niklas Adalberth, Founder and Chairman, Norrsken Foundation

NISK Capital Deals

NISK Capital, headquartered in Nairobi, specializes in seed-stage funding for SMEs across East Africa. The firm provides both capital and strategic advisory services to help startups scale. By January 2026, it was recognized as one of the top fintech investors in Rwanda.

One standout investment is BeneFactors Ltd., a Rwandan company offering working capital by purchasing unpaid invoices for immediate cash. This funding allowed BeneFactors to refine its services for SMEs that struggle with traditional bank financing, leveraging NISK Capital’s regional insights to identify untapped opportunities.

DOB Equity Commitments

DOB Equity, a Netherlands-based investor, focuses on scalable businesses with a social or environmental edge. The firm specializes in growth capital and private equity, targeting sectors like agriculture, healthcare, and financial services. They typically invest during seed and Series A rounds, bridging the gap between early-stage accelerators and larger growth funds.

Their strategy often involves backing businesses that combine multiple sectors. For instance, they support agtech platforms integrating financial services or healthtech companies embedding insurance solutions, aligning with Rwanda’s fintech evolution.

International Finance Corporation Backing

The International Finance Corporation (IFC) supports Series B rounds and debt financing to attract private investment in developing markets. Rather than focusing on startups, the IFC typically steps in when companies have validated their business models and are ready to expand regionally.

By providing large-scale capital, the IFC reduces risks for commercial investors, signaling market maturity. Their involvement ensures that Rwandan fintechs can secure funding at every stage of their development.

Next, we’ll compare these investors side by side to highlight their unique contributions.

Why Kigali Attracts Fintech Investment

Kigali has become a magnet for fintech investment, not because of its market size, but due to its forward-thinking regulations and strategic initiatives. The city’s approach allows fintech companies to launch and scale faster compared to its neighbors, creating a fertile ground for innovation.

Three key initiatives fuel this progress: the Rwanda Digital Acceleration Program (RDAP), the Fintech Strategy 2024-2029, and the Kigali International Financial Centre (KIFC). Together, these programs have turned Kigali into a hub for testing and deploying groundbreaking fintech solutions. Building on the success of earlier funding rounds, these initiatives are solidifying Kigali’s position as a leader in the fintech space.

Rwanda Digital Acceleration Program (RDAP) Impact

The RDAP focuses on creating a strong digital foundation to ease operations for fintech companies. Key components include a nationwide 5G rollout for reliable connectivity, the e-Kash system for seamless payment integration, and a digital ID system that simplifies Know Your Customer (KYC) processes.

This infrastructure has been a game-changer for fintech growth. For instance, the National Bank of Rwanda’s regulatory sandbox has admitted 17 companies to test innovative solutions, such as IT Consortium Rwanda’s Chango platform, which digitizes traditional savings groups.

In a major step toward regional integration, the National Bank of Rwanda and the Bank of Ghana signed a memorandum on February 25, 2025, to establish a license passporting framework. This agreement allows regulated fintechs to expand services like mobile money and remittances across borders without needing new licenses. By linking its modest domestic market to larger regional opportunities, Rwanda turns its size into an advantage.

Fintech Strategy 2024-2029 Incentives

Introduced in October 2024, this strategy aims to make Rwanda the "center of gravity" for fintech in Africa. The targets are ambitious: attract $200 million in investment, create 7,500 jobs, establish 300 fintech companies, and achieve an 80% adoption rate by 2029. The government also aspires to place Rwanda among the top 30 countries on the Global FinTech Index.

The financial incentives are equally bold. Qualified fintech headquarters enjoy a 0% corporate income tax rate, while priority ICT sectors benefit from a reduced 15% rate. Rwanda’s pro-business policies also remove barriers like foreign exchange controls, ownership restrictions, and profit repatriation limits. Licensing is streamlined, taking just 3–4 months compared to the 6–12 months typical in other African nations.

To bridge talent gaps, Rwanda has introduced two-year entrepreneurship and talent visas for foreign startup founders and remote workers.

"This strategy represents not just a policy document, but our country’s commitment to positioning Rwanda as a leading fintech hub in Africa." – Paula Musoni, Minister of ICT and Innovation

Kigali International Financial Centre (KIFC) Role

The KIFC provides a specialized regulatory environment for investment funds and special purpose vehicles. Fund establishment can take as little as two days, and licensing is completed within 30 days. The center ranks 3rd among African International Financial Centres and 2nd in Sub-Saharan Africa, according to the Global Financial Centre Index.

Tax benefits are another major draw. KIFC members pay a reduced 3% corporate income tax (compared to the standard 15% for funds) and enjoy 0% withholding tax on dividends, interest, and royalties. Rwanda also has 17 Double Taxation Avoidance Agreements, making cross-border transactions more efficient. Companies must meet "economic substance" requirements, such as maintaining a physical office in Rwanda with at least 30% Rwandan professional staff.

"KIFC is becoming the epitome of the transformative power of well-governed financial services." – Jean-Marie Kananura, Chief Investment Officer at Rwanda Finance Limited

KIFC has further strengthened Rwanda’s leadership in sustainable finance by adopting a National Green Taxonomy, making Rwanda only the second African country to implement such a framework. This comprehensive support system has positioned Kigali as a standout destination for fintech investors.

| Policy/Initiative | Key Benefit | Target/Outcome |

|---|---|---|

| Fintech Strategy 2024-2029 | Regulatory sandboxes & clear policy framework | 300 companies by 2029 |

| KIFC | 3% corporate tax & capital attraction | 25 investment funds domiciled |

| RDAP Infrastructure | 5G, Digital ID, e-Kash interoperability | 80% adoption rate by 2029 |

| NBR Licensing | Fast-track approvals in 3-4 months | Faster market entry vs. 6-12 months regionally |

| Tax Framework | 0% HQ tax / 15% ICT tax | Increased foreign direct investment |

Investor Comparison Table

Investor Overview

Rwanda’s fintech ecosystem is drawing attention from a diverse range of investors, including local boutique firms and global development finance institutions. Each investor comes with its own strategy, investment focus, and regional priorities. While some concentrate on Rwanda’s domestic market, others use Kigali as a launchpad for broader East African expansion.

The table below outlines key investments, funding stages, and geographic areas of interest for prominent investors. Early-stage backers like Norrsken Foundation and Bathurst Capital primarily focus on Pre-Seed and Seed funding, whereas institutions like the International Finance Corporation (IFC) lean toward growth-stage investments through debt and Series B financing.

| Investor | Key Rwanda Investments | Stage Focus | Geographic Emphasis |

|---|---|---|---|

| NISK Capital | BeneFactors | Seed | East African Community (EAC) |

| International Finance Corporation (IFC) | Undisclosed Fintech | Debt, Series B | Global Emerging Markets |

| Norrsken Foundation | Eden Care Medical | Pre-Seed, Seed | Sweden, Rwanda, Nigeria, USA |

| Bathurst Capital | Eden Care Medical | Pre-Seed | Rwanda |

| DOB Equity | Undisclosed Fintech | Seed, Growth Capital | East Africa (Kenya, Rwanda, Uganda) |

A closer look reveals distinct approaches. NISK Capital and DOB Equity aim to tap into the broader East African market, leveraging Rwanda’s cross-border license passporting framework with Ghana for smoother regional expansion. On the other hand, Bathurst Capital keeps its focus local, backing ventures in Rwanda’s wellness and health insurance fintech sector exclusively.

As of late 2024, Kigali Innovation City has facilitated $40 million in tech startup deals. This, coupled with Rwanda’s efficient 3–4 month licensing process, makes the country an attractive testing ground for fintech innovations before scaling to neighboring markets.

These investor strategies highlight how targeted funding and a regional outlook are shaping Rwanda’s fintech landscape.

Conclusion

Rwanda’s fintech sector is a shining example of how well-executed regulations can elevate smaller markets onto the global stage. The country’s focused approach has ignited a wave of funding and growth, with the Fintech Strategy 2024–2029 aiming for $200 million in investments and 7,500 new fintech jobs by 2029.

What sets Rwanda apart is its streamlined regulatory framework. The National Bank of Rwanda ensures unified oversight, completing licensing processes in just 3–4 months. Additionally, the February 2025 license passporting agreement with the Bank of Ghana allows fintechs to expand across borders without duplicating regulatory efforts. This positions Kigali as a launchpad for pan-African fintech solutions.

Investors are responding to this environment by channeling funds into platforms that align with Rwanda’s public infrastructure. These include the national ID system, the Mutuelle de Santé insurance scheme, and the Irembo e-government platform. This collaboration between public and private sectors has helped Kigali rise as a fintech hub, ranking 61st globally and 8th in Africa as of 2025.

Looking forward, Rwanda has its sights set on breaking into the Global FinTech Index’s top 30 by 2029 and attracting 300 fintech companies to its ecosystem. With mobile payment transfers growing by 57% in volume and 4G coverage now reaching over 96% of the population, the groundwork for sustained growth is firmly in place. The bigger question isn’t whether Kigali will continue to attract fintech investment, but how quickly other African nations will adopt Rwanda’s playbook of aligning policy, infrastructure, and investment opportunities. Kigali’s approach is proving to be a blueprint for driving fintech innovation across the continent.

FAQs

How do fintechs get licensed in Rwanda?

Fintech companies in Rwanda can secure a license through a straightforward process that usually takes around 3 to 4 months. This process is backed by a supportive regulatory framework, which includes fintech sandboxes and simplified licensing steps. These measures help businesses meet compliance requirements while encouraging innovation in the industry.

What is eKash and who can use it?

eKash is Rwanda’s real-time digital payment platform designed for instant money transfers between banks and digital wallets. With no fees or delays, it provides a fast and convenient payment solution. Open to consumers, businesses, and merchants across Rwanda, eKash ensures a smooth and accessible way to handle payments.

What tax incentives do fintech startups get in Kigali?

Fintech startups in Kigali benefit from appealing tax incentives. For those that meet certain investment and operational requirements, there’s a 0% corporate income tax rate – a significant boost for businesses aiming to establish themselves in the market. Additionally, a 15% corporate tax rate is available for other eligible investments, offering further support for growth in this dynamic sector.

Related Blog Posts

- 10 Investors Investing in African Fintech

- Fintech Funding in Africa: Regional Breakdown

- Early-Stage Fintech Funding Trends in Africa

- Rwanda Fintech Funding Boom: Why Investors Are Backing Rwanda’s Next Wave of Startups