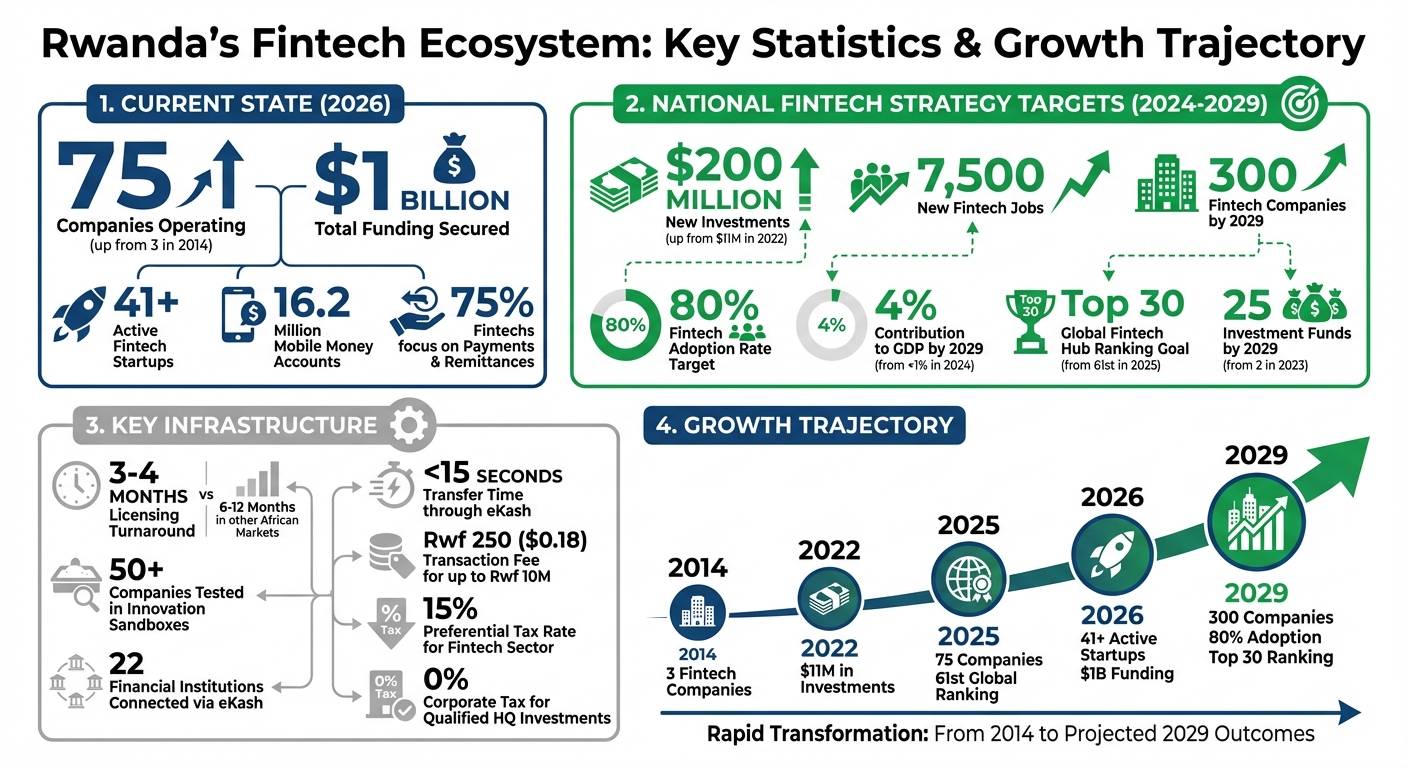

Rwanda’s fintech scene is booming, with over 41 active startups and $1 billion in funding as of early 2026. The country is positioning itself as a regional fintech hub, thanks to supportive policies like the Rwanda Startup Act and the Five-Year FinTech Strategy (2024–2029). These initiatives target $200 million in new investments, 7,500 jobs, and 300 fintech companies by 2029. Key infrastructure, such as Kigali Innovation City and faster licensing processes, further accelerates growth. Fintech companies are moving beyond basic financial services to focus on wealth-building tools, credit access, and embedded finance.

Here are 8 startups driving this transformation:

- Quiqpay: Focuses on digital payments and remittances, helping small businesses access financial services.

- Uplus: Digitizes savings groups and connects them to global contributors, with features like investment tools for retail investors.

- Bailport: Uses data-driven credit assessments to provide loans to small businesses without traditional collateral.

- ZEDI: Simplifies cryptocurrency-to-cash conversions and integrates business tools like inventory tracking.

- Kayko: Helps 8,500+ SMEs digitize operations, enabling cash-flow–based lending for underserved businesses.

- Exuus: Modernizes savings groups with its digital wallet and credit scoring tools, linking unbanked users to formal financial services.

- Eden Care: Rwanda’s first digital health insurer, combining health services with fintech solutions like preventative care tools.

- Tech In Africa: Provides real-time updates and insights about Rwanda’s fintech landscape, connecting startups with investors.

Rwanda’s fintech ecosystem is set to grow further, with goals like 80% fintech adoption and a 4% GDP contribution by 2029. With infrastructure upgrades, regulatory reforms, and incentives for startups, the country is becoming a launchpad for fintech innovation in Africa.

Rwanda Fintech Ecosystem Growth Statistics 2014-2029

Fintech innovation boosts financial inclusion, Rwanda to host inclusive Fintech Forum 2026

sbb-itb-dd089af

1. Quiqpay

There isn’t much public data available about Quiqpay, but it reflects the growth and potential of Rwanda’s digital payments sector.

Innovation in Financial Solutions

Rwanda’s fintech industry has been growing quickly, with a strong emphasis on payments and remittances. In fact, 75% of fintech companies in the country focus on these areas, working to address gaps in the payment infrastructure. This progress plays a key role in advancing financial inclusion.

Contribution to Financial Inclusion

Many of these payment-focused fintechs are tackling the financing challenges faced by small businesses. By using advanced data systems, they help banks evaluate creditworthiness without relying solely on traditional collateral. This approach makes formal financial services more accessible to entrepreneurs and small business owners who previously lacked options.

Scalability and Growth Potential

Supportive government programs, like Kigali Innovation City, provide resources to help fintech companies scale quickly. These initiatives strengthen Quiqpay’s ability to expand its services across the region.

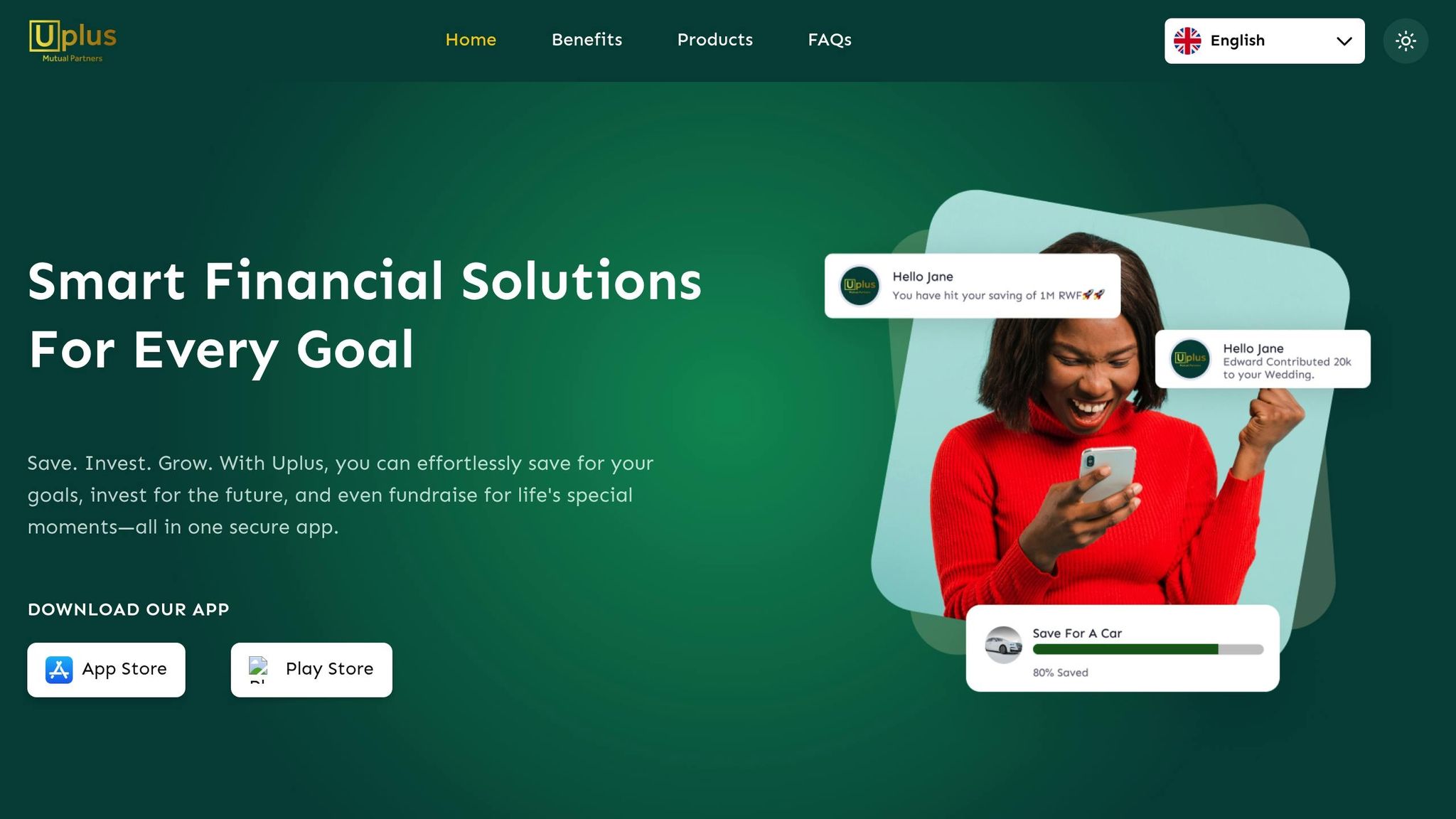

2. Uplus

Uplus transforms traditional savings groups, often used for weddings and funerals, into a digital platform. Founded in 2017 by Muhirwa Clement, the company secured Series A funding in January 2019 from East Africa Investments and employed 13 people as of July 1, 2024.

Innovation in Financial Solutions

Uplus is accessible across Android, iOS, and USSD, ensuring even users with basic feature phones can participate. By integrating Visa and Mastercard, it allows the Rwandan diaspora to join local savings groups from anywhere in the world.

"In Rwanda, saving money in a bank account is still unusual, so savings groups are common for important life events such as weddings and funerals." – East Africa Investments

In April 2024, Uplus introduced "Uplus for Investment" through the Capital Market Authority’s Fintech Regulatory Sandbox. This 12-month pilot connects retail investors, including university students, with Collective Investment Schemes. The initiative marks a shift from simple savings to wealth-building opportunities, reflecting Rwanda’s broader economic goals.

Contribution to Financial Inclusion

Uplus graduated from the Rwanda FinTecHub acceleration program in May 2021, earning milestone-based grants between $5,000 and $20,000. The platform focuses on Village Saving and Loans Associations (VSLA), digitizing these informal community groups while respecting their cultural significance.

Scalability and Growth Potential

Currently ranked as the top player in Rwanda’s group savings market, Uplus is well-positioned for regional growth. Its multi-channel support – spanning Android, iOS, and USSD – combined with Visa and Mastercard integration, connects traditional savings groups with global contributors and retail investors, paving the way for broader financial inclusion.

3. Bailport

Bailport addresses a critical economic challenge in Rwanda: the multi-billion-dollar financing gap that hinders small businesses. By using data-driven methods, the company evaluates creditworthiness without relying on traditional collateral requirements, offering a fresh approach to business financing.

A New Way to Assess Credit

At the heart of Bailport’s strategy is its focus on creating strong data systems. The company has introduced micro-ERP platforms designed to assist informal merchants with tasks like bookkeeping, inventory tracking, and tax reporting. These tools generate real-time financial data that lenders can use to make smarter, more informed credit decisions. Beyond simplifying daily operations, this system helps merchants build credible financial profiles, making it easier for them to secure funding.

Expanding Access to Financial Services

Rwanda’s National FinTech Strategy (2024–2029) highlights fintech as a key driver for increasing financial access and fostering socio-economic progress. Bailport aligns with this mission by opening doors to financial services for those traditionally excluded from the banking system. Through the digitization of informal merchants’ operations, Bailport is helping integrate these businesses into the formal financial ecosystem, bridging the gap between underserved communities and essential financial resources.

4. ZEDI

ZEDI tackles a key hurdle in the cryptocurrency world: making digital currencies practical for everyday use. The platform allows users to instantly convert major cryptocurrencies like Bitcoin (BTC), Ethereum (ETH), and USDT into local currency. From there, they can easily transfer funds to mobile money wallets or bank accounts. This approach moves beyond just trading crypto – it transforms digital assets into tools for paying bills and covering daily expenses. By simplifying crypto-to-cash conversions, ZEDI opens the door to broader utility payments and enterprise applications.

Innovation in Financial Solutions

One of ZEDI’s standout features is its integration with utility payments. Users can settle bills for electricity, internet, and TV subscriptions directly from their converted crypto balance – all within a single platform. The mobile app, available on both the App Store and Google Play, operates around the clock, offering responsive customer support, low fees, and transparent exchange rates. This makes managing finances both simple and efficient.

Scalability and Growth Potential

ZEDI, also known as Zed Payments, expands its reach through its Zed 360 platform, a comprehensive business management tool. This platform combines inventory tracking, point-of-sale systems, eCommerce, and automated accounting into one streamlined solution. It’s designed for industries like education, transportation, and consumer goods. For example, Zed Transport facilitates trackable mobile payments for public service vehicles, ensuring clear income and expense records. Meanwhile, the inventory system provides real-time stock updates, automatic low-stock alerts, and sales forecasts based on past trends. These features eliminate the need for manual bookkeeping and bring efficiency to business operations.

Impact on Rwanda’s Fintech Ecosystem

ZEDI is more than just a transaction platform – it’s a tool for transforming how businesses operate across multiple sectors. By integrating enterprise-level features like automated invoicing and financial reporting, the platform supports small businesses with tools to generate journals, trial balances, and profit-and-loss statements. This robust financial infrastructure not only simplifies operations but also helps businesses position themselves for growth and access to formal financing. ZEDI is playing a pivotal role in advancing Rwanda’s fintech landscape by embedding these advanced financial tools into everyday business processes.

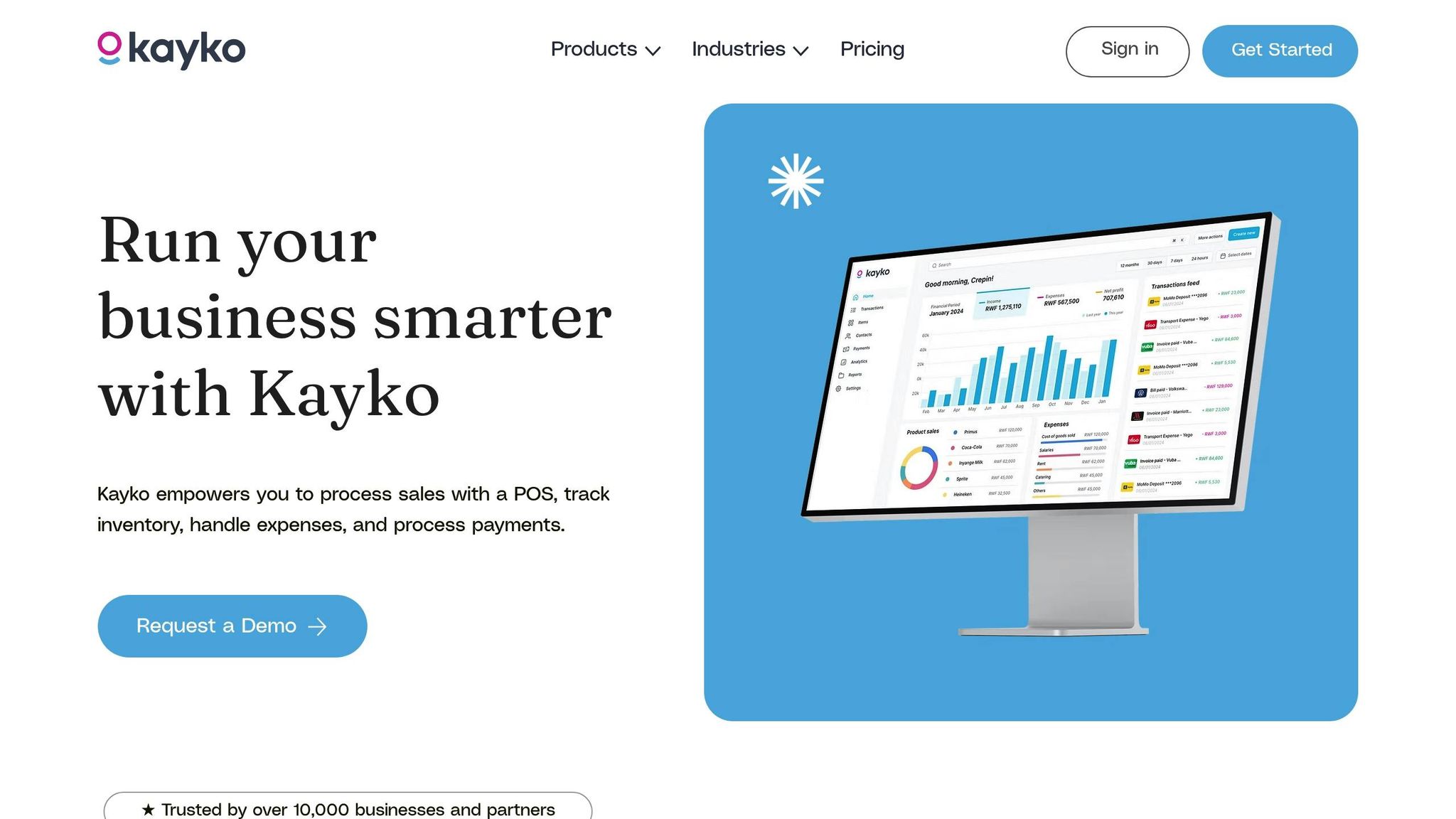

5. Kayko

Kayko is tackling one of Rwanda’s biggest economic hurdles: the $1.2 billion financing gap faced by small and medium-sized enterprises (SMEs). Founded in 2021 by brothers Crepin and Kevin Kayisire, the startup was inspired by a personal experience – their mother struggled to secure a bank loan for her catering business due to the lack of formal financial records. This mission aligns with Rwanda’s broader efforts to bring informal businesses into the formal financial system, paving the way for greater digital financial inclusion in the SME sector.

Rethinking Financial Tools for SMEs

Kayko operates as a micro-ERP platform, designed to digitize the operations of informal merchants like neighborhood kiosks, salons, and small retail shops. Its tools simplify bookkeeping, inventory tracking, and tax compliance by transforming chaotic cash flows into organized digital profiles. For businesses previously overlooked by traditional banks, Kayko provides a lifeline. As the company explains:

Millions of SMEs across Africa run their businesses every day, but have no usable financial data to grow, borrow, or scale.

Bridging the Financial Gap

Kayko’s platform captures real-time business activity through its point-of-sale and bookkeeping features, enabling merchants to prove their creditworthiness without needing traditional collateral. Currently supporting over 8,500 Rwandan SMEs, the platform turns everyday transactions into credit profiles that enable cash-flow–based lending. This approach shifts the focus from collateral-heavy lending models to ones based on actual business performance, opening up formal financing opportunities for previously unbanked businesses.

Driving Growth and Expansion

In January 2026, Kayko secured $1.2 million in seed funding from investors such as Burrow Capital, LuxDev, and Hanga Ignite. This funding is being used to enhance the platform’s infrastructure to handle higher transaction volumes and to develop proprietary credit scoring models. These tools allow financial institutions to assess SME creditworthiness using real-time data rather than relying on traditional collateral. Kayko is also expanding its collaborations with banks and microfinance institutions to offer working capital loans tailored to SMEs’ needs.

Shaping Rwanda’s Fintech Future

Kayko’s work aligns closely with Rwanda’s National Fintech Strategy (2024–2029), which aims to position Kigali as a financial hub for the region. By evolving from a simple digitization tool to a full-fledged financial intermediation platform, Kayko is playing a key role in formalizing Rwanda’s informal sector. Its data-driven lending model could serve as a blueprint for similar initiatives across East Africa, marking a significant step forward in the region’s fintech landscape.

6. Exuus

Exuus is transforming Rwanda’s traditional Village Savings and Loan Associations (VSLAs) by introducing digital solutions. Founded in 2014 and headquartered in Kigali, the company created the SAVE platform – a secure digital wallet and decentralized ledger that replaces the old-fashioned metal cashboxes. Designed to work on both feature phones via USSD and smartphones, the platform ensures accessibility even in rural areas. During a 2018 pilot with World Vision Rwanda and Care International Rwanda, 27 VSLAs, comprising over 800 members, adopted the platform. Some groups managed to save over $2,000 digitally – a testament to its effectiveness.

Modernizing Financial Practices

Exuus has reimagined traditional savings methods with its SAVE platform, which secures deposits and loan repayments through mobile money. By eliminating the need for physical cashboxes, it reduces risk while offering free transactions and automated SMS receipts. The platform supports all Rwandan mobile money providers and operates in both Kinyarwanda and English, making it widely accessible.

Another standout feature is Cartix, a proprietary credit scoring algorithm developed by Exuus. This tool uses savings group activity to create digital profiles for unbanked individuals, helping connect them to formal financial services. CEO Shema Steve explained:

In rural Africa, banks are seen as exclusive and non-lucrative. We created a beneficial bridge connecting marginalized communities with the formal financial market.

Driving Financial Inclusion

By 2020, Exuus had reached 20,000 users and set its sights on expanding to one million. Like other pioneers in Rwanda’s fintech industry, the company uses technology to promote inclusivity and open up new lending possibilities. Operating on a subscription model, Exuus charges VSLAs a monthly fee per user. It also offers a lending-as-a-service platform, enabling banks and financial institutions to connect with unbanked communities using its infrastructure and credit scoring data. Recognized for its impact, Exuus has received approval from the National Bank of Rwanda and won second place at the Hanga Pitchfest 2022, earning a $20,000 prize.

Scaling for the Future

Exuus is gearing up for a Series A funding round to expand its operations beyond Rwanda. So far, the company has raised $170,000, including $120,000 in its most recent round in late 2025. With Rwanda’s savings group market valued at $64 million and the East African market surpassing $2 billion in annualized savings, the growth potential is immense. The company’s data analytics tools also allow NGOs and practitioners to monitor VSLA activities in real time, further enhancing its value. Positioned as a key player in Rwanda’s digital finance sector, Exuus is paving the way for broader advancements in financial inclusion and innovation.

7. Eden Care

Eden Care stands out as Rwanda’s first digital health insurer, seamlessly blending fintech with healthcare. Founded by Moses Mukundi, the company operates with a small but efficient team of 28 employees. Unlike the traditional insurance providers burdened by paperwork and manual processes, Eden Care has embraced digital tools at its core. It offers an HR Dashboard for employers and a Mobile App for members, creating a user-friendly and efficient system that redefines how health insurance is managed in Rwanda.

Innovation in Financial Solutions

Eden Care’s digital-first strategy simplifies the insurance experience for both employers and members. The HR Dashboard helps employers manage benefits with ease, while the Mobile App gives members direct access to services and a personalized concierge team. This streamlined approach eliminates much of the complexity typically associated with health insurance.

In February 2026, the company introduced ProActiv, a preventative care service aimed at addressing wellness proactively. ProActiv includes mental health evaluations, fitness assessments, and screenings for conditions like heart disease, stroke, cancer, and diabetes. This was a groundbreaking step, as it marked the first time a Rwandan insurer prioritized prevention and early detection over reactive care.

Contribution to Financial Inclusion

By digitizing its processes, Eden Care has opened the door for smaller businesses and younger, tech-savvy users who were often left behind by traditional, paper-heavy models. Founder and CEO Moses Mukundi highlighted this shift, saying:

We are contributing to a more inclusive insurance ecosystem in Rwanda by working with a diverse range of stakeholders and recognizing the unique problems and opportunities they present.

This approach has made health insurance more accessible and practical for groups that might otherwise struggle to participate in the system.

Impact on Rwanda’s Fintech Ecosystem

Eden Care demonstrates how fintech can extend beyond banking and payments to transform critical sectors like healthcare. As a member of the HealthTech Hub Africa network, the company is part of a larger pan-African push toward integrated digital services. By focusing on preventative care and leveraging data for smarter decision-making, Eden Care is helping shift Rwanda’s insurance model from reactive treatment to one centered on long-term wellness and sustainability. Designed to be both affordable and comprehensive, Eden Care ensures that essential health services are within reach for more people.

8. Tech In Africa

Tech In Africa stands as Rwanda’s go-to platform for fintech news and analysis. With a community of over 77,800 followers, it provides real-time updates on startup funding, regulatory shifts, and advancements in technology. By highlighting key data – like the $1 billion in total funding secured by Rwanda’s startup ecosystem – the platform not only attracts foreign venture capital but also fosters transparency, enabling smarter decision-making. This clarity forms the backbone of its offerings.

Driving Change Through Financial Solutions

Tech In Africa addresses the demand for reliable and timely information about startups. One standout initiative is its dedicated WhatsApp channel, which delivers instant updates on startup developments, funding announcements, and technological advancements directly to users’ mobile devices. Additionally, the platform produces detailed reports on funding patterns and digital transformation, building a robust data framework that aids investors in making informed choices.

Strengthening Financial Inclusion

The platform shines a spotlight on Rwandan fintech startups working toward financial inclusion, such as Exuus. By amplifying their visibility, Tech In Africa connects these startups with investors, partners, and customers who might otherwise miss out on Rwanda’s growing fintech landscape. This exposure is particularly critical for early-stage companies that lack large marketing budgets. By helping these startups gain recognition, Tech In Africa nurtures the ecosystem and encourages broader participation in the market.

Supporting Rwanda’s Fintech Ecosystem

Acting as a knowledge hub, Tech In Africa bridges the gap between startups, investors, and policymakers. Its coverage of topics like digital transformation, mobile money innovations, and regulatory updates equips stakeholders with the insights needed to navigate the market and seize opportunities. For Rwanda’s emerging fintech sector, this platform not only documents the industry’s journey but also fosters learning and collaboration. By enabling data-driven decisions, Tech In Africa complements the groundbreaking efforts of Rwanda’s fintech startups and strengthens the ecosystem as a whole.

What’s Next for Rwanda’s Fintech Industry

Rwanda has set its sights on becoming "Africa’s FinTech center of gravity" with an ambitious five-year National FinTech Strategy (2024–2029). The plan aims to attract $200 million in investments, a sharp rise from just $11 million in 2022, and achieve an 80% fintech adoption rate among its population. It also envisions significant growth in the number of fintech companies and job creation, supported by regulatory reforms and infrastructure advancements.

Regulatory innovation is a cornerstone of this transformation. The National Bank of Rwanda (NBR) has cut the licensing process to a 3-4 month turnaround, a stark improvement over the 6-12 months typical in other African markets. Innovation sandboxes operated by the NBR and the Capital Market Authority have already helped over 50 companies test their solutions. Additionally, Rwanda has introduced "license passporting" frameworks through agreements with central banks in Ghana and Tanzania, enabling fintechs to expand across borders without redundant licensing requirements.

"Rwanda is not competing on size, but on agility and strategic positioning, providing a launchpad for FinTechs planning to conquer the broader African market." – Jean Claude Nshimiyimana, Corporate and Legal Services Lead, Andersen in Rwanda

Infrastructure upgrades are also driving growth. The eKash interoperable payment system connects 22 financial institutions, enabling transfers in under 15 seconds with fees as low as Rwf 250 (about $0.18) for amounts up to Rwf 10 million (roughly $7,300). Meanwhile, the ongoing 5G rollout and national digital ID system are reducing customer acquisition costs and enabling instant KYC verification. Rwanda has also linked with Tanzania’s instant payment system to facilitate regional remittances.

For investors and entrepreneurs, opportunities extend well beyond payment systems. Key growth areas include insurance, personal finance management, and government-to-person transactions. The Kigali International Financial Centre offers attractive incentives, such as a 15% preferential tax rate for fintech and ICT sectors, and a 0% corporate income tax rate for qualified headquarters investments. To further support startups, the Development Bank of Rwanda plans to launch a debt fund in Q2 2026, offering non-dilutive capital tailored for early-stage tech ventures. Additionally, new two-year entrepreneurship and talent visas are available for foreign founders and remote workers to address local skill shortages.

Rwanda aims to climb from 61st in 2025 to the top 30 fintech hubs globally by 2029. The government projects the fintech sector will contribute 4% to GDP by 2029, up from less than 1% in 2024. The number of investment funds domiciled in Rwanda is expected to grow from just 2 in 2023 to 25 by 2029. With these initiatives, Rwanda is positioning itself as a testing ground for fintech innovation and a launchpad for startups targeting the broader African market. This evolving ecosystem offers immense potential for pioneering companies to drive both financial inclusion and technological advancement.

Conclusion

Rwanda’s fintech sector has experienced extraordinary growth, expanding from just 3 active companies in 2014 to over 75 by 2025 – a transformation that highlights the nation’s rapid progress in less than a decade. The startups mentioned here, such as Quiqpay with its payment solutions, Kayko’s data platform supporting over 8,500 SMEs, and Eden Care’s advancements in health insurance, are all contributing to Rwanda’s ambitious goal of achieving 80% fintech adoption by 2029. These companies are not just innovating – they’re making financial services more accessible, from digitizing VSLAs to enabling cash-flow lending for small businesses, particularly in rural areas.

This shift signals a broader evolution in Rwanda’s financial sector. It’s no longer just about financial inclusion but about what comes next. As Martin Mbonu, CEO of ComzAfrica, aptly puts it:

Financial inclusion was the foundation, not the destination. After people are financially included, what next?

The next step is wealth creation. While 75% of fintech startups focus on payments and remittances, other areas like insurance, personal finance, and government-to-person transactions remain largely untapped, offering fertile ground for innovation.

For investors, Rwanda represents a promising opportunity. Between 2014 and 2023, the country secured over $1 billion in startup funding across more than 80 deals. Looking ahead, government initiatives aim to attract an additional $200 million for fintech by 2029.

Entrepreneurs can take advantage of resources like the National Bank of Rwanda’s regulatory sandbox to pilot new ideas and collaborate with telecom operators, leveraging the country’s 16.2 million mobile money accounts. Innovation hubs like Norrsken House Kigali and Kigali Innovation City also provide mentorship and networking opportunities, further strengthening the ecosystem. These efforts reflect Rwanda’s comprehensive approach to fintech development, blending regulatory flexibility, infrastructure investment, and ecosystem support.

The goal of creating 7,500 fintech jobs by 2029 isn’t just an economic milestone – it underscores Rwanda’s potential to become a launchpad for financial innovation across the continent.

FAQs

How can U.S. investors back Rwandan fintech startups in 2026?

U.S. investors looking to back Rwandan fintech startups in 2026 have several opportunities to explore. They can join funding rounds, such as seed or Series B stages, to provide crucial financial support. Collaborating with organizations like the Norrsken Foundation or IFC, which focus on Rwanda’s fintech ecosystem, offers additional avenues to get involved.

Key growth areas in Rwanda’s fintech scene include embedded finance, mobile money, and digital lending. These sectors are already making a significant impact, with startups collectively processing over $5 billion in loans. The potential for further expansion is clear, making it an exciting time for investors to engage.

How do Kayko and Bailport qualify SMEs for loans without collateral?

Kayko provides a way for small and medium-sized enterprises (SMEs) to secure loans without needing collateral. It achieves this by leveraging data-driven platforms that help businesses digitize their operations. By doing so, lenders can assess an SME’s creditworthiness using digital records like sales, inventory, taxes, and payment histories.

On the other hand, Bailport operates as a multi-currency e-wallet, enabling instant money transfers. However, it does not specify how it qualifies SMEs for collateral-free loans.

What does Rwanda’s “license passporting” mean for fintech expansion?

Rwanda’s “license passporting” system offers fintech companies a straightforward way to expand their operations across borders. If licensed in one participating country, they can operate in another without jumping through extensive regulatory hoops. This approach cuts down on compliance challenges, makes entering new markets easier, and encourages smoother cross-border activities. It’s a step that promotes growth and stronger partnerships within the fintech industry.

Related Blog Posts

- Top 5 Startups to Watch in Côte d’Ivoire in 2025

- Top 5 Startups to Watch in Kenya in 2025

- Rwanda Fintech Funding Boom: Why Investors Are Backing Rwanda’s Next Wave of Startups

- Rwanda Fintech Funding 2026: Key Deals, Investor List, and Why Kigali Is Winning